Usio offers integrated payment solutions trusted by industries like lenders, SaaS, developers, non-profits, utilities, government agencies, card issuers, and more. With billions in transactions, Usio is a proven leader in fintech ensuring the most secure, simple, and cost-effective payment experience possible.

Our products provide a seamless experience for both you and your customers. With Integrated Payments, ACH, Card Issuing, and Print & Mail available in one complete package, Usio can take your business to the next level.

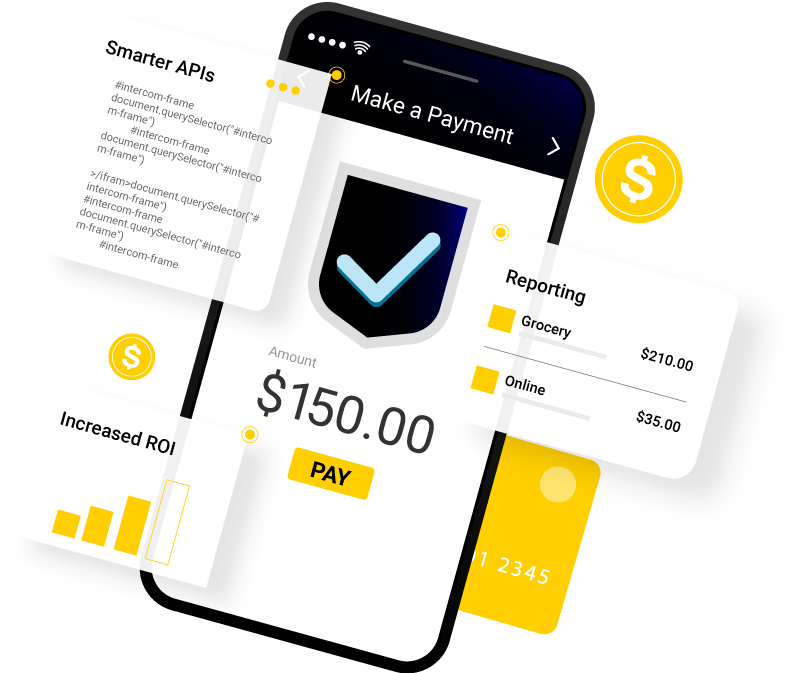

Integrated Payments

Usio provides Payfac-as-a-service, streamlining monetization for ISVs and delivering comprehensive payment solutions to their software users.

Our products provide a seamless experience for both you and your customers. With Integrated Payments, ACH, Card Issuing, and Print & Mail available in one complete package, Usio can take your business to the next level.

Integrated Payments

With no investment cost, and utilizing the highest level of security on the market, Usio Integrated Payment Solution APIs will drive meaningful revenue in 30 days or less.

The most cost-effective way for same-day and next-day payments. Usio, Nacha Certified Third Party Sender, also offers PINLess Debit, Remotely Created Checks, Account Validation, Prenotes and more.

Usio Akimbo Prepaid card solution empowers businesses, nonprofits, and government entities to effortlessly create and manage disbursements for a variety of needs.

Usio significantly reduces costs and time by providing a single platform that allows recipients to select how they receive payments. They can opt to have funds deposited directly into their bank account, transferred to their debit card, or receive a printed check.

Usio processes payments online, in-person, or by phone, including credit cards, checks, and ACH, for faster transactions. Combined with our Document Composition, Warehousing, Printing and Mailing Services, Usio is the perfect partner for a turnkey solution that guarantees you’ll get paid faster.

Your one-stop solution for organizations reliant on printing and mailing. From invoices to checks, Usio covers it all for utilities, healthcare, credit unions, banks, governmental agencies, and manufacturing. Combined with Usio eBill Presentment and Payment for the best solution on on the market.

Create a hybrid, all-in-one payment and funds disbursement solution by combining Usio products. Streamline costs and save time by consolidating all payment vendors into one integrated platform.

Our products provide a seamless experience for both you and your customers. With Integrated Payments, ACH, Card Issuing, and Print & Mail available in one complete package, Usio can take your business to the next level.

Integrated Payments

With no investment cost, and utilizing the highest level of security on the market, Usio Integrated Payment Solution APIs will drive meaningful revenue in 30 days or less.

Your one-stop solution for organizations reliant on printing and mailing. From invoices to checks, Usio covers it all for utilities, healthcare, credit unions, banks, governmental agencies, and manufacturing.

Create a hybrid, all-in-one payment and funds disbursement solution by combining Usio products. Streamline costs and save time by consolidating all payment vendors into one integrated platform.

Making Payments Seamless for Over Two and a Half Decades.

Unwavering Security

Elevate your confidence with the utmost in security measures. At Usio, we process all payments with an unwavering commitment to excellence, utilizing the highest security standards, including PCI Level 1 and tokenization.

Our dedication to safeguarding extends beyond payments. Printing and mailing data benefit from the robust protection of SOC II security standards. Usio’s comprehensive SOC security plan covers all facets of our operations and production, ensuring the safeguarding of corporate data, computing networks, plant infrastructure, and personnel. When it comes to security, choose the best – choose Usio.